When comparing the cost of pet insurance, customers sometimes feel caught off guard by the price compared to what they pay for their own health insurance. In these circumstances, confusion might lead to skepticism and cause people to wonder, "Is pet insurance worth it?"

That’s why it’s essential to understand how pet insurance works, as the process is typically different from the traditional structure most are familiar with.

To help you shop with confidence, we're answering some of our customers' frequently asked questions to clarify the key differences between insurance for pets and insurance for people. You can also use the links below to jump to the specific information you're looking for.

Table of Contents:

- Pet insurance doesn't work like human health insurance

- Is pet insurance expensive?

- Why do people get pet insurance for their dogs and cats?

- Key Takeaways

Pet insurance doesn’t work like human health insurance

Pet health insurance is designed to help you financially prepare for the unexpected by offsetting unforeseen veterinary costs.

We believe that pets are people and see them as our furry, four-legged family members. However, in the eyes of the law, pets are legally considered property. Therefore, pet insurance is more similar to car insurance or renters insurance, rather than human health insurance.

What does that mean in practice?

- No “networks” to worry about. While some pet insurance companies offer vet-direct pay, they all offer the option to reimburse you. That means your coverage will work at any vet.

- No open enrollment periods to worry about. You can enroll or change your coverage at any time.

- Significantly cheaper premiums. You’ve probably seen most human health insurance plans costing $300+ a month. With pet insurance, these premiums average around $49/month for dogs and $28/month for cats (see average pet insurance costs by breed, age, and state).

Alas, no pet insurance will cover pre-existing conditions. Though some will cover curable conditions after a certain waiting period with no recurring symptoms. Also, while the specific pre-existing condition won’t be covered, any new injuries or illnesses will be covered - so pre-existing conditions don’t exclude you from being eligible for all coverage (see options for pre-existing conditions).

Available plans

There are two types of pet insurance plans, each covering separate categories of veterinary services:

- Accident-Only (AO) coverage, which includes costs exclusively related to unexpected pet injuries such as bite wounds, torn ligaments, broken bones, foreign object ingestion, and more.

- Accident & Illness (AI) coverage, which includes the costs required to treat pets who are injured and/or sick. AI policies are more common because they offer comprehensive financial protection against possible illnesses that may arise at any point in your pet’s future — including chronic conditions, hereditary diseases, common infections, rare disorders, and more. However, most pet insurance providers allow you to choose which type of coverage you want to enroll your pet in, allowing you to find a solution that works best for your budget.

NOTE: Many pet insurance companies also offer optional wellness plans for routine pet care. By adding this additional level of coverage as a “rider” to your pet insurance policy, you can offset the cost of preventive pet care, including the cost to spay/neuter dogs, microchip your pet, stay current on dog vaccinations, and so forth.

In contrast, insurance plans for humans involve a network of doctors and hospitals, typically known as a Health Management Organization (HMO) or Preferred Provider Organization (PPO).

In-network vs. out-of-network providers

Many people are required to stay within a (sometimes limited) network of doctors, specialists, and treatment facilities to receive covered medical care.

Pet insurance isn’t limited to HMO or PPO networks. You have the freedom to go to any licensed veterinarian you like, anywhere in the country. Once you get your bill, submit it to your insurance provider to get reimbursed.

Premiums and deductibles

Both human and pet insurance plans include premiums (what you pay to maintain your insurance policy, typically on a monthly basis) and deductibles (the amount of money you must pay for treatment out-of-pocket before your insurance policy will kick in and cover expenses).

The difference is that human health insurance plans operate on a “managed care” model while pet insurance operates on a “fee-for-service” model.

Essentially, that means human health insurance companies will pay your provider directly (once you cover your deductible). Alternatively, pet insurance companies will reimburse you for claimed expenses on covered costs (after your deductible is met), but you are required to pay for the entire veterinary bill before filing a claim.

Pro Tip: One way to take advantage of this is to pay the bill on a credit card with great reward points. This way you accrue the credit card rewards and the pet insurance company reimburses you to pay off the card before the next statement (to see how long each company takes to reimburse, compare top plans here).

Copays vs. reimbursements

With a human health insurance policy, you’re usually required to pay a flat fee upfront at the time of service. This is your copay. After you pay it, the service provider will bill your insurance company for the remainder of the cost, which can sometimes lead to disputes or unwelcome surprises if certain costs aren’t covered.

In contrast, pet insurance requires you to pay for the vet bill upfront and out-of-pocket, then file an insurance claim to get reimbursed for (a portion) of the treatment costs. You can easily file a claim online or in the app, and experience fast payment times ranging between a couple of days and a couple of weeks.

NOTE: This structure is beginning to change, as some companies like Pets Best now offer Vet Direct Pay.

Access to coverage

Pet insurance companies don’t limit your access through “open enrollment” periods. You can enroll and unenroll from your pet insurance policy at any time. (Keep in mind, however, there is usually a mandatory waiting period before your policy kicks in once you’ve enrolled that you may be subject to upon re-enrollment).

This makes it easier for senior cats and dogs to obtain pet insurance for older pets because they don’t need to meet special conditions — they can just sign up. Additionally, unlike humans, pets can’t lose their coverage just because they age, either.

Coverage for pre-existing conditions

However, a pet insurance company can still deny insurance coverage for a pet's pre-existing condition. Human health insurance providers in the U.S. stopped being able to deny coverage of pre-existing conditions in 2014 due to changes in healthcare law.

If you enroll your pet into a health insurance policy and they've already been diagnosed with an illness or injury, you won't be able to get coverage for the cost to treat it. That's why it's so important to enroll your pet when they're still young.

Is pet insurance expensive?

Pet insurance is a good deal, but some plans may seem expensive when compared to the rate some people pay for their personal health insurance. Here's some context that helps explain the price disparity.

The government heavily subsidizes some health insurance rates

Some people may qualify for subsidized health insurance from the government. They may pay a small amount or nothing at all out of pocket for care. This makes health coverage more accessible for everyone, but it can also hide the true cost of an insurance plan.

Similarly, some people may purchase health insurance through state and federal healthcare exchanges at a subsidized rate. They may pay only a fraction of their monthly premiums, while the government pays the rest.

This can make human healthcare seem relatively inexpensive compared to pet insurance, as there are no subsidies for pet insurance.

Employers often pay for some (or all) of their employees' insurance premiums

Many employers are generous with their health insurance benefits. They might pay half or even all of the cost of their employees' health insurance plans. Employees who have to pay part of the cost usually don't have to think about it much, as the cost is taken from their paycheck automatically.

By contrast, most employers don't offer to pay for the cost of pet insurance. However, this is also beginning to change, as more companies and HR departments choose to offer pet insurance as an employee benefit.

Most veterinarians don't want to take part in a "managed care" healthcare model

It can take weeks or months for doctors, dentists, dermatologists, and similar healthcare providers to receive reimbursement from insurance companies. This process can be frustrating, especially for owners of smaller clinics that have tight margins.

These types of managed care plans could provide patients with more affordable care, but they don't offer enough incentives for veterinarians. They aren't typically an option if you want pet insurance.

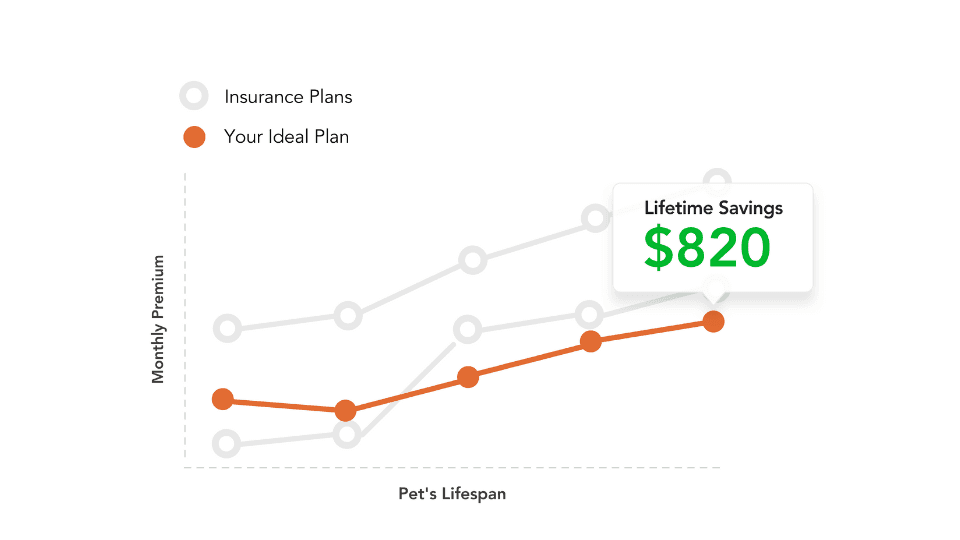

Unlike Pawlicy Advisor, some brokers increase the price per policy sold

Another factor that can increase pet insurance rates is the potential fee assessed by the insurance broker selling the pet insurance policy. In today's society, many consumers buy pet insurance indirectly through a licensed insurance agent online. Some brokers might skew recommended plans toward the most profitable choice rather than the most suitable for the buyer.

Pro Tip: When comparison shopping with Pawlicy Advisor, all rates quoted are guaranteed to be the lowest possible price. Also, our integrity is important to us and the veterinarians we work with, so our recommendations are not financially biased. When we analyze your pet and recommend a plan, that recommendation is based on objective data around your pet’s breed-specific health risks, age, and location.

Why do people get pet insurance for their dogs and cats?

Pets are members of the family and they deserve the best care. But when pets are young and healthy, paying for a pet insurance policy might seem like an unnecessary cost to some.

Unfortunately, this type of thinking sometimes puts pet parents in an impossible position when they're faced with an unexpected vet bill they can't afford. They have to choose between getting their pet the care they need and paying a bill they can't afford, or forgoing their pet's care so they don't lose all their money.

Pet insurance prevents this scenario from happening in the first place. You do have to pay your veterinarian up-front before getting reimbursed, but you can do so knowing that you'll be able to afford your other monthly bills. Many pet parents manage this by keeping a credit card on hand for emergencies.

Of course, the most common reason pet owners buy pet insurance is to get peace of mind. They know that if their pet gets sick or injured, they'll be able to get them all the care they need to get well again.

Key Takeaways

- Pet insurance works differently than human health insurance. It reimburses the pet parent rather than paying the veterinarian directly, so there are no "in-network" or "out-of-network" veterinarians to worry about.

- People get pet insurance to protect themselves from high vet bills, but they also buy it to make sure their pets can get the care they need when they need it. Pet insurance provides peace of mind.

- You can enroll or change your coverage at any time.

- Pet insurance will not cover pre-existing conditions.

At Pawlicy Advisor, we understand the importance of making well-informed decisions, especially regarding personal finances. We believe it should be easy for pet parents to give their pets the best care possible.