How To Use Pet Insurance Without The Stress (PCSR Method)

How do I use pet insurance to protect my pet and save on vet bills?

Think of it like auto or renters insurance: you are buying peace of mind and protection against costly surprises. Unlike human health insurance, you don't need to find doctors within your pet insurer's network! You can use your pet insurance policy at any licensed veterinarian in the U.S.

In this guide, we'll walk you through the PCSR method, how to Prepare, Claim, Submit, and Reimburse, so you can use your pet insurance effectively and stress-free.

This article is written for two kinds of pet parents:

- Those who already have pet insurance and want to know how to use it to file claims and get reimbursed quickly.

- Those who are still exploring their options and wondering how pet insurance works before they buy a plan.

Key Takeaways

- By choosing the right policy for your pet’s breed and age, you can maximize the value of your coverage.

- Most pet insurance claims will need to use the PCSR method (Prepare, Claim, Submit, and Reimburse)

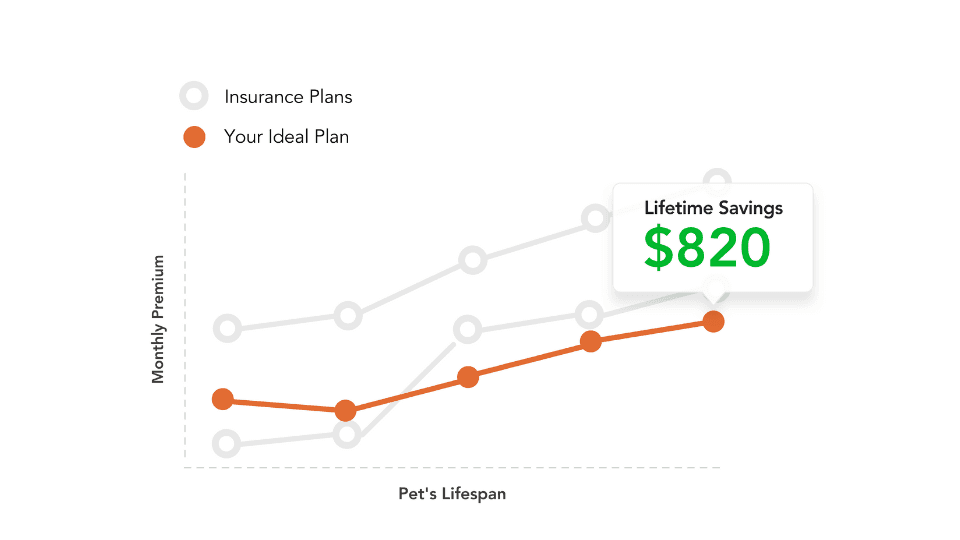

- Pawlicy Advisor makes it easy to compare plans and find the ideal fit based on your pets’ unique needs and your budget.

Compare Top Pet Insurance Companies Side-by-Side

Use Pawlicy Advisor to get personalized quotes from leading brands and see how each plan stacks up — instantly.

100% free to use. No fees. No commitment.

These simple steps will help you maximize the benefits of your policy.

How Pet Insurance Works

If you are just searching for how pet insurance works, keep reading. We will guide you through the basics of enrollment, filing a claim, and maximizing your coverage.

If you already have pet insurance and are wondering how to file a claim and get reimbursed quickly, skip to the next section for tips on maximizing your policy.

Enrollment

Make Sure Your Policy Makes Sense For Your Breed, Location, Age, And Any Pre-Existing Conditions. Before signing up for a pet insurance plan, consider your pet's unique needs. Some plans are customized for specific breeds, while others may have exclusions based on your pet's age or medical history. Be sure to review the fine print for any restrictions that may affect coverage for pre-existing conditions your pet may already have.

For example, large breeds may have different coverage options for joint injuries, while certain locations may have fewer insurance options available. It's crucial to align your policy with these factors to avoid surprises down the line.

Are there pet insurance policies where you don’t have to pay upfront?

While most pet insurance companies require upfront payment to the veterinary practice at time of treatment, some insurers can pay the veterinarian directly for certain procedures if pre-approved (Note: Some insurers require veterinarians to be in their 'Network' in order to pay the veterinarian directly). It's worth considering this option when evaluating insurers, as it can alleviate the immediate financial burden.

What Is A "Monthly Premium" & "Deductible" In Pet Insurance?

Your monthly premium is the amount you pay regularly for your pet’s coverage, and it typically varies based on factors like your pet’s breed, age, and health status.

A deductible is the portion of the veterinary bill you're responsible for before your plan’s reimbursement takes effect. Most pet insurance companies offer an annual deductible. Some insurance companies offer a per-incident deductible, meaning if the same injury occurs more than once in future years, the deductible will no longer apply.

Common deductible amounts include $100, $250, $500, or $1,000, though some providers may offer options as high as $1,500 or more. A lower deductible usually means higher monthly premiums, while a higher deductible can reduce your monthly cost but requires you to cover more upfront when an emergency occurs before your coverage kicks in. The right choice depends on your pet’s health history, your budget, and how much financial risk you’re comfortable taking on.

Coverage: What Does Pet Insurance Cover, What It Doesn’t

Pet insurance typically covers unexpected accidents, illnesses, and often chronic conditions, but there are exclusions. Most plans do not cover routine care, such as vaccinations or wellness exams, unless you have an add-on wellness plan.

It's essential to understand what each policy covers and the exclusions to avoid unexpected costs.

What Are "Limits", And How Are They Different Than "Annual Limits?"

Limits are generally counted as "per-incident" or “per condition” (whereas annual limits refer to a total for the year) and are something you should investigate when comparing pet insurance options as you anticipate how much and what type of veterinary care your pets might need for their ages and conditions. Per-incident or per-condition limits cap how much you can be reimbursed for a single illness or accident. If surgery, lab tests, medications, and follow-up care all total $5,000 and your limit is $2,000, then you are responsible for the difference ($5,000 - $2,000 = $3,000).

NOTE: Not sure what type of care your unique pet might need? Use Pawlicy Advisor to scan hundreds of pet insurance policy variations and find the right plan at a great price.

What Do I Need To Know About My Annual Limit?

Annual limits refer to what amount your insurance coverage is capped at. In other words, the dollar amount you can be reimbursed for in one year.

Once you hit your plan’s annual reimbursement limit, you are responsible for paying vet bill costs until your coverage resets for the year.

Depending on your pet, you may not hit the annual limit. The good news is that many pet health insurance options have unlimited annual limits!

Does A Wellness Plan Count As An Insurance Policy?

A wellness coverage plan is separate from your standard accident and illness insurance plan. Wellness coverage does not cover unexpected illness or injury (so no cancer treatment or any urgent care needs). Instead, your wellness plan will help reimburse toward routine care and some preventive care (like vaccinations). It's particularly helpful for new puppy or new kitten appointments.

What Is My Reimbursement Rate?

Your reimbursement rate is the amount a pet insurance company pays you back for the cost of care. A typical reimbursement can range anywhere from 60% to 100% of the bill. The most comprehensive pet insurance plans will reimburse 80% to 90% of your total vet bills.

For example, if your vet bill is $1,000 and you have an 80% reimbursement rate, your insurer will pay you back $800 (after the deductible is met). Plans with higher reimbursement rates typically cost more each month, but they increase how much of the vet bill you get reimbursed for in the event of unexpected accidents or illnesses.

Does Pet Insurance Cover Surgery?

Yes, pet insurance can cover surgery, but the extent of coverage depends on your plan’s terms. Surgical procedures, including emergency surgeries, are usually covered under most accident or illness policies. However, be sure to check your specific policy for exclusions or caps on certain procedures.

Pre-existing Conditions, End of Life Care & Euthanasia

Most pet insurance plans do not include coverages for pre-existing conditions or any treatment recommended for them.

Similarly, many plans exclude end-of-life care and euthanasia, but some providers may cover the costs under certain conditions. Always read the fine print and check whether your provider includes these scenarios in their coverage.

Does Pet Insurance Cover Vaccines?

No, pet insurance usually does not cover vaccinations or other routine preventative care, unless you have a wellness plan. These plans are separate from the basic insurance policy and are designed to help with regular health maintenance for your pet.

When I Get Pet Insurance, How Soon Can I Use It?

Once you have enrolled, there is usually a waiting period before you can use your pet insurance. This can range from a few days to a few weeks, depending on the provider and the type of coverage. Be sure to check the waiting periods outlined in your policy to avoid any surprises.

How To Use Pet Insurance & Get Claims Paid Fast

To ensure you receive your claims promptly and without hassle, remember the acronym PCSR: Pay, Collect, Submit, Reimburse.

Pay Your Vet After Your Pet’s Care

Most pet insurance providers reimburse you directly, so you will need to pay your vet at the time of treatment. Using a credit card can help you cover costs upfront and then pay them off with your reimbursement, often before your statement is due.

Some insurers, however, offer direct pay to veterinarians. If avoiding upfront costs is important, be sure to check whether your insurer offers this option.

Collect All Documents Like Invoices

Smooth claims depend on accurate paperwork. Always collect detailed invoices, medical records, and receipts from your vet. Many insurers now simplify this process with mobile apps, allowing you to snap photos of receipts and upload them instantly. This reduces errors, saves time, and speeds up the approval process.

Submit Your Claim

Once you have the necessary documents, submit your claim as soon as possible. Most providers allow online or in-app submissions, which are faster than mailing forms. Double-check the information before submitting to avoid delays.

Get Your Claims Reimbursed

Reimbursements typically take anywhere from a few days to two weeks, depending on your provider and the complexity of your claim. Some companies are faster than others. Many Pawlicy Advisor users report seeing reimbursements in under a week with top-rated insurers. The key is submitting complete, accurate claims right away.

Which Pet Insurance Is Easiest To Use?

Understanding pet insurance can be challenging, but some insurers make it easier to use, especially when it comes to filing claims and receiving reimbursement quickly.

“Most insurance carriers are pretty easy to submit claims with. I'd say the criteria for “easiest to use” might include a mobile app or online submission option to submit claims, as well as offer alternative claim submission options like mail, email, or fax.” - Kari Steere, Licensed Insurance Producer

Below, we have highlighted the top 3 easy-to-use pet insurance companies that make the process as smooth as possible:

Pet Insurance Company | Claim Process | Reimbursement Speed |

|---|---|---|

Pumpkin | Claim submission options for website, mobile app, and email submissions are available. | Timely reimbursements (often within 5–10 days) |

Spot | Accept claims through their website, via mail, email, fax, and their mobile app. | Fast reported claim reimbursements (2-4 days) |

Prudent Pet | Options for online, mail, email, and fax claim submissions are available. | Reported claim turnaround time of 1-7 days |

These companies prioritize speed, simplicity, and various options for claim submission to ensure that you get your claims processed without unnecessary delays. Their apps and online portals make it easy for pet owners to file claims, track reimbursements, and manage policies with minimal hassle.

Compare Top Pet Insurance Companies Side-by-Side

Use Pawlicy Advisor to get personalized quotes from leading brands and see how each plan stacks up — instantly.

100% free to use. No fees. No commitment.

Get peace of mind with Pawlicy Advisor

Pet insurance gives you peace of mind and the ability to make the best choices for your pet’s care without worrying about the financial burden. By working closely with your vet and choosing the right policy for your pet’s breed and age, you can maximize the value of your coverage.

If you are not sure your current plan is the right fit, Pawlicy Advisor makes it easy to compare top-rated companies across all categories. Use our free comparison tool to find a customized plan tailored to your pet and budget.

CEO & Co-Founder - Pawlicy Advisor

Woody Mawhinney, CEO and Co-Founder of Pawlicy Advisor, was relieved when his pet insurance covered his Shar Pei’s monthly prescription costs. However, many veterinarians and pet parents in his community shared with him the difficulties they faced when evaluating options. As a licensed insurance producer nationally, he launched Pawlicy Advisor as the first U.S. pet insurance marketplace actively endorsed by veterinarians, aiming to improve the pet insurance experience by providing objective analysis, more thorough comparison, and a streamlined educational experience.

Do you want to find the best pet insurance?

Let's analyze your pet's breed, age, and location to find the right coverage and the best savings. Ready?

Analyze My PetAbout Pawlicy Advisor

Recommended by the American Animal Hospital Association and veterinarians nationwide, Pawlicy Advisor makes buying the best pet insurance easier. We compare top brands and match you to the right protection at a great price. Our free service has helped over 1 million happy pet owners.

More you might like

Guides

When Pet Insurance Is Worth It